Even Better Insurance

What is Medicare Part D?

What is Part D?

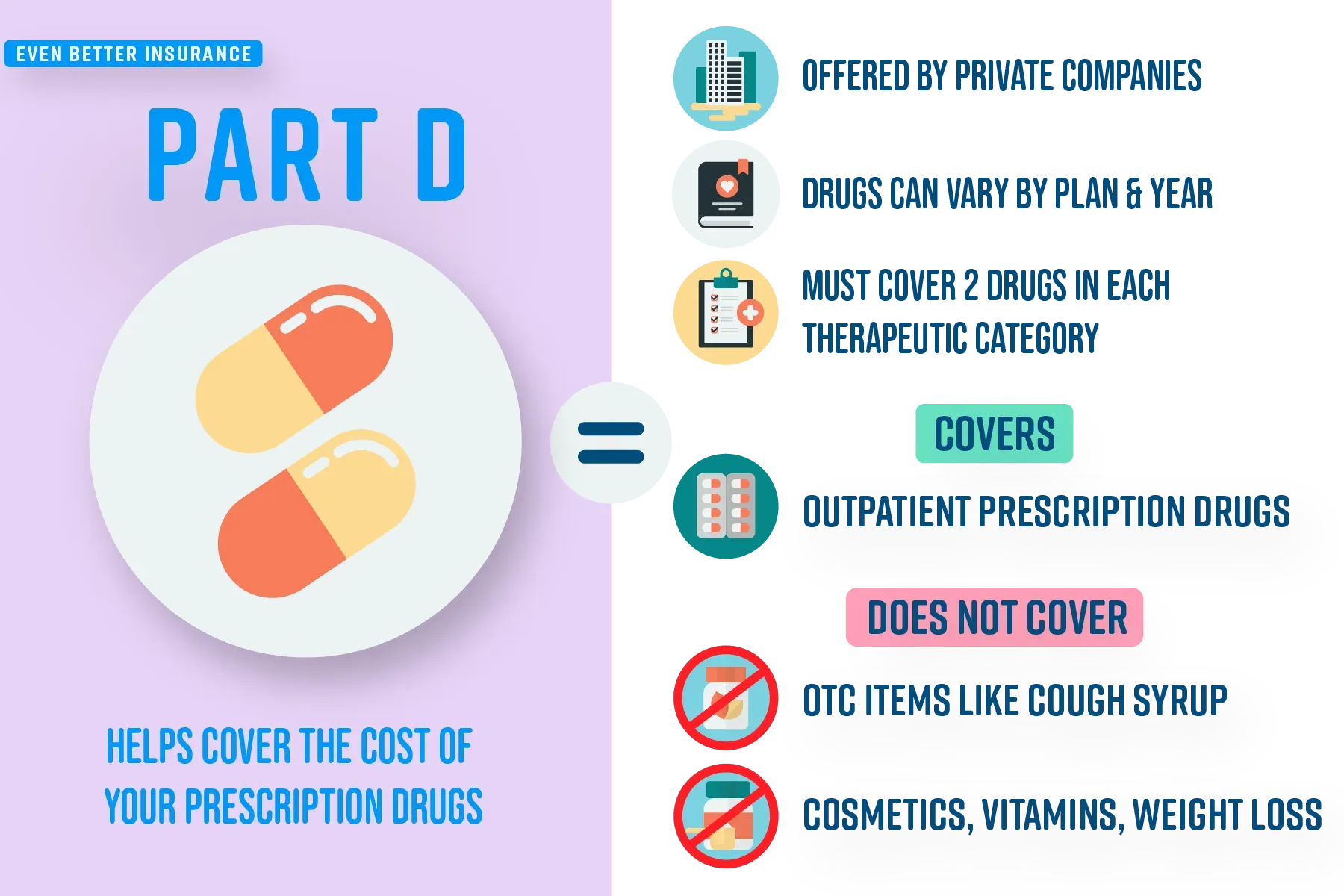

Part D is known as Medicare prescription drug coverage. It is an important part of the federal Medicare program and was created in order to help cover the costs of prescription drugs, which have long been a source of financial ruin for Medicare beneficiaries. Part D plans are offered by health insurance companies and other private companies that must abide by the rules set forth by Medicare.

Part D covers:

- Outpatient prescription drugs. However, some drugs may be actually covered under Part B (medical insurance (link to Part B)) instead of Part D. Drugs covered under other Parts of Medicare and not Part D tend to be drugs that you cannot administer yourself - things like nebulizer solutions administered via a nebulizer machine, chemotherapy, most injections and infusions and more. You can see a list here (https://www.medicare.gov/coverage/prescription-drugs-outpatient).

Part D does not cover:

- over-the-counter medications like cough syrup or antacids.

- some prescription drugs, such as Viagra, when it is used for erectile dysfunction; medicines used to help you grow hair; medicines that help you gain or lose weight; or most prescription vitamins.

Quick Links

How do you get Part D?

There are two ways you can get Part D prescription drug coverage:

- You can buy a stand alone Part D plan to compliment your Original Medicare (and Medicare Supplement if you purchase one).

- You can join a Medicare Advantage plan that includes prescription drug coverage.

Browse Page

When Are You Eligible to Get Part D?

You can enroll in a Part D plan:

- When you first become eligible for Medicare, you can join during your Initial Enrollment Period (link to enrollment periods).

- If you get Part A and Part B for the first time during the General Enrollment Period (link to enrollment periods), you can also join a Medicare drug plan from April 1– June 30. Your coverage will start on July 1.

- You can join, switch, or drop a Medicare drug plan between October 15– December 7 each year. Your changes will take effect on January 1 of the following year.

- If you’re enrolled in a Medicare Advantage Plan, you can join, switch, or drop a plan during the Medicare Advantage Open Enrollment Period, between January 1–March 31 each year (link to enrollment periods).

- If you qualify for a Special Enrollment Period (link to enrollment periods)

Browse Page

How Does Part D Coverage Work?

Part D plans work by helping you cover the costs of prescription drugs.

Whether you purchased a stand alone Part D plan, or joined a Medicare Advantage plan that included Part D coverage, each company puts together its own list of the drugs it covers for that year, known as a ‘formulary’. They must abide by basic rules set by Medicare to ensure adequate coverage for you. All the drugs on a formulary are divided up into ‘tiers’. The price you will pay for a drug will depend on its ‘tier’, with lower tiers generally being cheaper generic drugs and higher tiers being more expensive brand-name and specialty drugs.

When you go to fill your prescriptions, you will need to make sure that you do so at one of your drug plan’s ‘preferred’ network pharmacies in order to receive the lowest advertised copayment and coinsurances. Many companies’ ‘preferred’ networks include large pharmacies such as CVS, Walgreens, Rite-Aid, Wal-Mart and more.

The actual costs you pay can include premiums, deductibles, copayments, and coinsurances. Depending on the number of prescriptions you are taking and the cost of those drugs, throughout the year though you may experience a change in the prices you pay and your out of pocket costs. This is known as the ‘coverage gap’ or commonly referred to as the ‘prescription drug donut hole’ (more detailed info on this here (insert link to Donut hole)).

There may also be certain limitations to which of your drugs are covered, the quantity you can refill at one time, you may even be subject to step therapy to certify your need for the highest cost specialty or brand name drugs etc...

Browse Page

How Are Part D Plans Structured?

As with all other Medicare plans and coverage options, it is important to understand how Part D coverage is structured, in order to minimize any unwanted surprises and help you effectively plan. First, we’ll highlight how coverage for drugs is determined, then we will talk about how costs will be structured.

What Determines My Drug Coverage?

Formulary: A formulary is a publicly available list of every drug that the Part D plan covers for that year. This list can change throughout the year, however the changes must be approved by Medicare and the Part D plan must notify you if they make changes. You will also receive a document every fall explaining the changes for the upcoming year.

All part D companies formularies’ must cover at least 2 drugs in each therapeutic category and most include all drugs in these 6 categories: antidepressants; antipsychotics; anticonvulsants; immunosuppressants for treatment of transplant rejection; antiretrovirals; and antineoplastics; except in limited circumstances.

This is a vital tool when shopping for Part D coverage because you should only consider joining a Part D that includes coverage for the drugs you need or are taking. Otherwise you will have to try to request a coverage exception which can be denied.

Tiers: Each drug on the formulary is assigned to a specific tier. Each tier determines what you will pay in copayments, or if there is a deductible you must meet first, etc. Each company sets their own drug tiers, which means that different companies may cover the exact same same drug at different prices. Generally speaking, the lower the tier, the cheaper a drug will be and vice versa.

Generic drugs vs Brand-name drugs. What's the difference?

We get questions on this topic from our clients regularly. However, we are not pharmacists and our advice is not in any way intended to be a substitute for professional medical advice. The difference as it relates to your prescription drug coverage is as follows:

Most prescription drug plan formularies break up their drug tiers into subsections of generics and brand name drugs based on the prices which the plan negotiates with manufactures for those covered drugs.

Each plan may be different, so we always recommend checking the tier list. An example of a tier list may look like this:

Tier 1 - Preferred Generic

Tier 2 - Non-preferred Generic

Tier 3 - Preferred Brand

Tier 4 - Non-preferred Brand

Tier 5 - Specialty

Generic drugs: These drugs are copies of brand-name drugs. The Food and Drug Administration (FDA) ensures that generic drugs have the exact same: active ingredient, dosage form, safety, strength, route of administration, quality, performance characteristics and intended use as their brand-name counterparts.

‘Preferred’ Brand-Name Drugs: These are drugs for which no generic is currently available. They have been on the market for a while and are widely used.

‘Non-preferred’ Brand Name Drugs: These are more expensive brand-name drugs than ‘preferred’ because these drugs have recently come on to the market. In most cases a preferred alternative medication is available for this.

‘Specialty’ Drugs: ‘Specialty’ drugs are defined by Medicare as being any drug that costs over $670 per month. These are the most expensive drugs and can result in thousands of dollars per year in out of pocket costs (unless you have prescription drug assistance also known as ‘extra help’). There are over 30 specialty drugs available and not all are covered by Part D plans.

Though your goal may be to save as much on prescription drug costs as possible, there are times when generic drugs are not an exact or suitable substitute for their brand-name counterparts, especially when there is no generic drug available. Keep that in mind when evaluating each prospective drug plan’s formulary and tier list. So even though you may not be taking any drugs now, or are currently only taking generics, we always recommend budgeting for the cost of a few brand name drugs in the future as a way to further protect you from unexpected large costs.

Costs

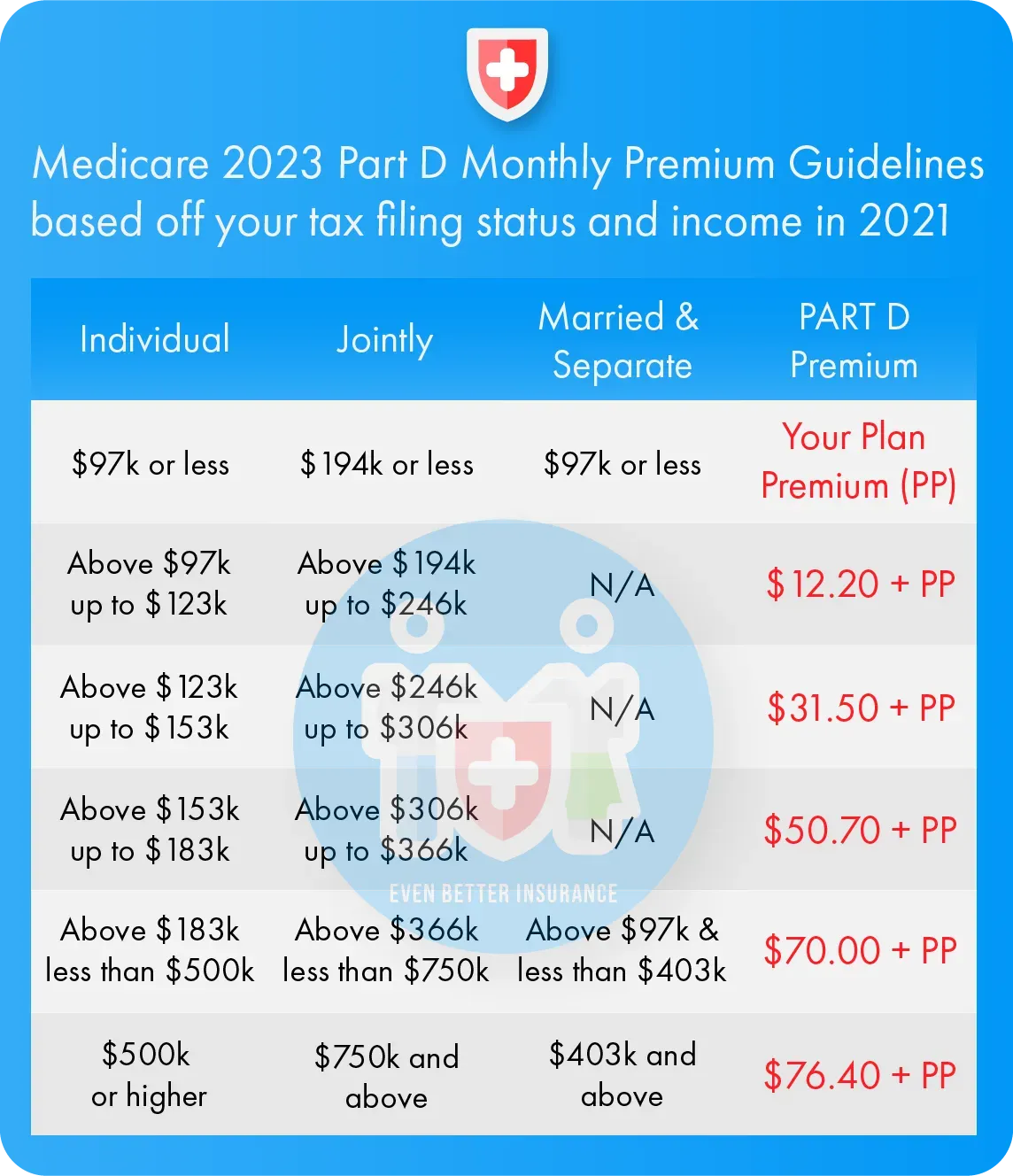

Premiums: If you buy a stand alone Part D plan, the national average monthly premium in 2023 is $32.74. If you receive Part D coverage as part of your Medicare Advantage plan then the cost of your Part D coverage is already included in your Medicare Advantage plan’s monthly premium.

You may also pay a higher premium if your income is above a certain level ($97,000 if you file individually or $194,000 if you’re married and file jointly).

Yearly Deductible: This is the amount you must pay before your drug plan begins to pay its share of your covered drugs. Some drug plans don’t have a deductible.

Copayments and Coinsurance: These are the amounts you pay for your covered prescriptions after the deductible (if the plan has one). You pay your share and your drug plan pays its share for covered drugs. If you pay coinsurance, these amounts may vary throughout the year due to changes in the drug’s total cost. Your copayment amount for your drugs will vary based on each drug’s tier rating.

Though the elements that typically comprise ‘cost’, such as premiums, deductibles, copayments and coinsurance work similarly to other types of Medicare coverage, determining what you’ll actually pay out of pocket every year for your drug coverage is more complicated!

That is because of there are 4 ‘stages’ of prescription drug coverage:

- The Annual Deductible

- Initial Coverage

- The Coverage Gap or ‘Donut hole’

- Catastrophic Coverage

We go over each of the coverage stages and talk about the coverage gap or ‘donut hole’ in detail here.

Browse Page

Part D Late Enrollment Penalty

After your Initial Enrollment Period (link to enrollment periods) is over, if you go for longer than 63 days without getting a Part D plan or if you do not have creditable prescription drug coverage (coverage from an employer or union that pays at least as much as Medicare standard prescription drug coverage) then you will be assessed a Part D late enrollment penalty. You will have to pay this penalty every month that you have Part D coverage for the rest of your life.

How much is the Part D Late Enrollment Penalty?

The penalty is calculated by multiplying 1% of the “national base beneficiary premium” ($32.74 in 2023) by the number of full, uncovered months that you were eligible but didn’t join a Medicare drug plan and went without other creditable prescription drug coverage. The final amount is rounded to the nearest $.10 and added to your monthly premium. Since the “national base beneficiary premium” may increase each year, the penalty amount may also increase each year. After you join a Medicare drug plan, the plan will tell you if you owe a penalty and what your premium will be.

Example: Mrs. Roberts was first eligible for Medicare in June of 2020. She didn’t have prescription drug coverage from any other source and didn’t see the need for a plan because she wasn’t taking any prescription drugs. In November of 2022, she finally joined a Medicare drug plan, and her coverage began on January 1, 2023.

Since Mrs. Roberts was without creditable prescription drug coverage from October 2020–December 2022, her penalty in 2023 is 26% (1% for each of the 26 months) of $32.74. (the national base beneficiary premium for 2023), which is $8.51. The final amount is rounded to the nearest $.10, so she’ll be charged $8.50 each month in addition to her plan’s monthly premium in 2023. She’ll continue to pay a penalty for as long as she has Part D coverage, and the amount may go up each year.

Here’s the math: 26 months without coverage (.26 or 26% penalty) × $32.74 (2023 base beneficiary premium) = $8.51.

$8.50 = Mrs. Martin’s monthly late enrollment penalty for 2023 (rounded to the nearest $.10)

Here at Even Better Insurance

we’ve helped clients who’ve gone even longer than Mrs Roberts without coverage to understand why Part D coverage is important and to, in some cases, appeal their late enrollment penalties.

Appealing the Part D Late Enrollment Penalty

Let’s face it, sometimes things fall through the cracks, or details are accidentally omitted from your records. We’ve seen clients who have been penalized even though they did have creditable coverage, so it only took them appealing their penalty and showing proof of their creditable coverage for their penalty to be rescinded. Your mileage may vary though.

If you are subject to a penalty, you will receive a notice from your plan within the first few weeks of joining the plan that informs you of your late enrollment penalty. Once you receive that notice, you have 60 days (there should be an exact date that you need to respond by listed on that notice) to request a ‘reconsideration’ of your penalty. Your plan should provide you with this reconsideration request form, you may need to call your plan’s member services hotline if you need help.

Browse Page

Common Part D Questions

I don’t currently take or plan on taking any drugs. Why should I sign up for a Part D plan?

Prescription drug costs are one of the leading causes of financial difficulty for Medicare beneficiaries. So, although getting prescription drug coverage is technically optional, we strongly recommend getting coverage as soon as you are eligible. We recommend this for two simple reasons:

- To avoid a Part D late enrollment penalty. You will essentially be ‘throwing away’ this much money every single month for the rest of your life to pay an easily avoidable penalty. If you are concerned about drug plan premiums, our ‘Even Better’ Medicare plan experts can help you find the lowest cost monthly premium that will offer at least basic coverage because...

- You can’t predict the future. We’ve had clients come to us who, for one reason or another, delayed getting prescription coverage until it was too late, and now are stuck with hefty late enrollment penalties. In some of the worst cases, they waited until they were prescribed expensive life saving drugs to sign up for coverage, but because there are enrollment periods, they were forced to pay thousands of dollars out of pocket while they waited for their coverage to start.

Need help choosing a Part D plan? Not sure if you are eligible? Worried about a possible late enrollment penalty?

Let our ‘Even Better’ Medicare plan experts guide you!

Browse Page