Even Better Insurance

Types of Medicare Advantage

Medicare Advantage plans can be a great way to get extra coverage while cutting costs. There are several types of Medicare Advantage plans! While they may have common cost structures and familiar terms, the main differences lie in the types of networks they use or the qualifying conditions to enroll. For instance, some plans use a PPO style network which is generally more broad and eliminates the need for assigning a Primary care physician, while some use a more traditional HMO network. Some plans may only accept if you have been diagnosed with a chronic condition or receive assistance from Medicaid. However, all of these plans are run by private health insurance companies contracted with the federal government and abide by rules set by Medicare.

Enrolling in a Medicare Advantage plan means your Medicare benefits will be administered through the Medicare Advantage plan rather than through Medicare itself for however long you are enrolled in the plan (in other words you are not permanently replacing your Medicare).

To enroll in any of these Medicare Advantage plans, you must continue to keep your Part A and Part B active - in other words you must continue to pay your Part A (if any) and Part B monthly premiums to the government or you will be dis-enrolled!

Read on to find out which type may be right for you!

Quick Links

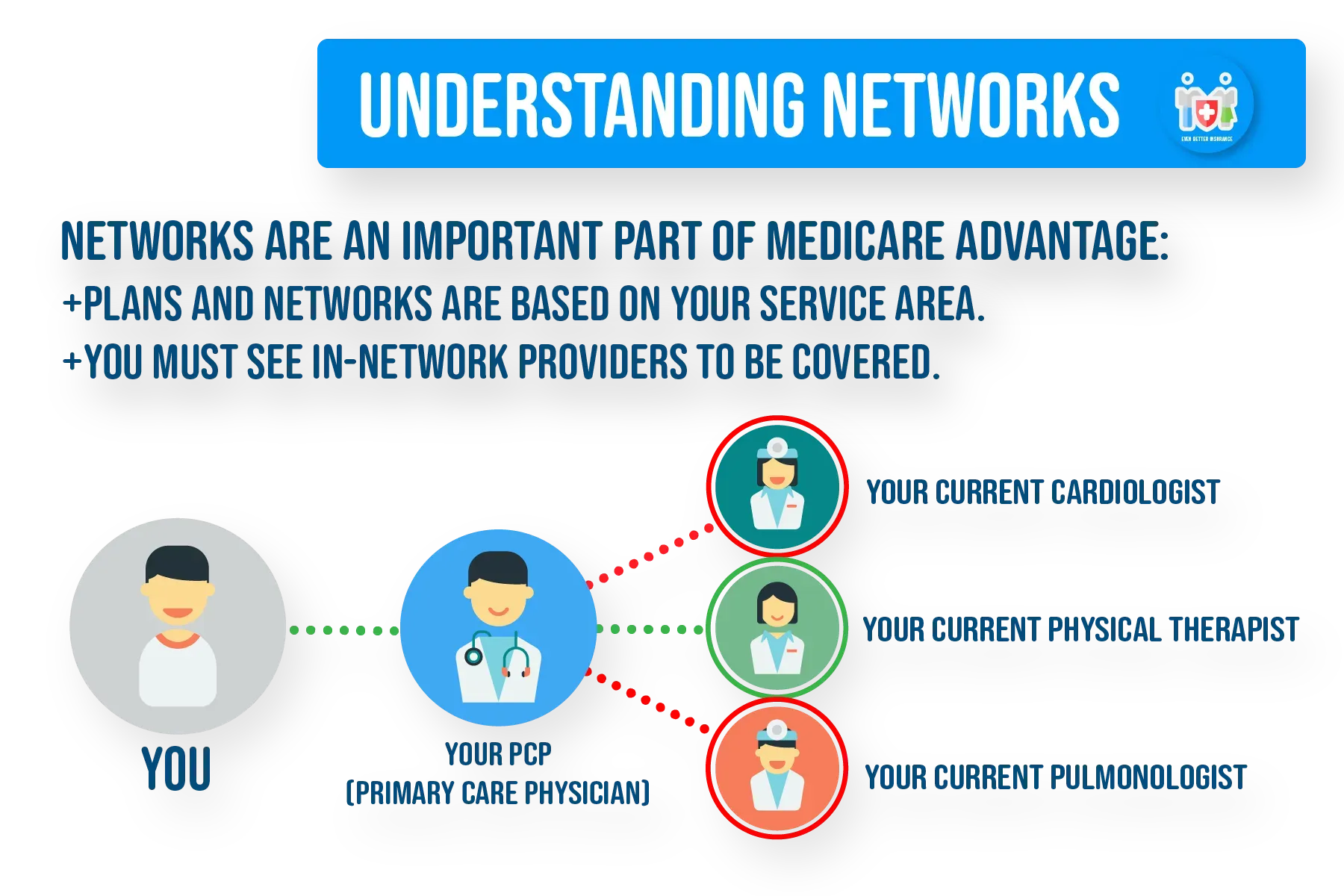

Medicare Advantage HMO

Medicare Advantage HMO is the most popular type of Medicare Advantage plan. These category of plans are commonly referred to as ‘managed care’ or ‘health maintenance organizations’. These plans require that you receive your care through a network of doctors and hospitals contracted with the health plan you choose.

When you enroll you must choose a Primary Care Physician (also known as a ‘PCP’). PCP is just another term for your main internist or family care doctor. The PCP is an important component in the HMO system because they act as your gateway to the rest of your care. For instance, if you need non-emergency treatment from a specialist doctor (cardiologist, pulmonologist etc), in many cases you will need your PCP to submit a referral for you first before you see them. Some services and plans may not require these referrals however.

In many cases, the doctors, hospitals and equipment providers within your network can be identified out ahead of time to help you eliminate worry or confusion.

Here are some Pros and Cons of Medicare Advantage HMO:

PROS

- Low to no monthly premiums. Many plans have $0 monthly premiums.

- Lowest copayments compared to other plan types.

- Maximum out of pocket limit to keep your costs low every year.

- Local network of physicians and hospitals.

- Most include Part D prescription drug coverage at no premium per month.

- Additional benefits beyond what Original Medicare covers.

- Vision, Dental, Hearing, Over the Counter Health items, Fitness Memberships, Acupuncture, Chiropractic, Private Transportation, and more.

- PCP will have constant access to updated consolidated Rx list to help avoid issues like over prescription of medications between all your specialists.

CONS

- Most in-network care limited to service area (except for Emergency, Urgent Care, Dialysis).

- Subject to referrals, approvals.

- Benefits beyond Original Medicare are subject to change year to year.

Browse Page

Medicare Advantage PPO

Medicare Advantage PPO (Preferred Provider Organization) plans can be a great alternative to both Original Medicare and a Medicare Advantage HMO because they can offer things like a yearly maximum out of pocket limit, prescription drug coverage and low copayments that Original Medicare doesn’t offer, while also giving you access to a wider network of providers and eliminating the need for a designated PCP that Medicare Advantage HMOs often require.

Your overall premiums, deductibles, copayments, coinsurance, will most likely be more than on an HMO plan however, and Medicare Advantage PPOs typically don’t offer the same amount of additional health and wellness benefits that Medicare Advantage HMO’s offer while still having certain rules and restrictions from the PPO health plan.

Here are some Pros and Cons of Medicare Advantage PPO:

PROS

- Larger networks and ability to see out-of-network providers (for a higher rate).

- Lower monthly premiums than a Medicare Supplement (Medigap).

- Some additional benefits beyond what Original Medicare covers.

- Most include Part D prescription drug coverage.

- Most eliminate need for a PCP and referrals, approvals.

- Maximum out of pocket limit to keep your costs low every year.

CONS

- Higher premiums, deductibles, copayments, coinsurance, than Medicare Advantage HMO.

- Still subject to network (albeit a slightly larger one than HMO).

- Maximum out of pocket is likely higher than on HMO.

Browse Page

Medicare Advantage PFFS

Medicare Advantage PFFS (Private Fee For Service) plans are somewhat less common plans and generally require you, the member, to do more legwork on your own compared to HMO and PPO plans. The reason for that is because some PFFS plans do not have set network of providers while some have a very large set network of providers, so it is up to you as a patient to determine ahead of time with the doctor if he/she will accept the rate that your Medicare Advantage PFFS plan pays. If the doctor does not accept the rate that your health plan pays for services, then those services may not be covered.

Just like HMOs and PPOs, you will still have to abide by certain rules and regulations of the health plan and will have premiums, deductibles, copays, coinsurance set by the health plan. Some plans even include Part D prescription drug coverage.

While less popular, a Medicare Advantage PFFS plan can be a good option for someone who wants the nationwide freedom to see doctors while traveling but who does not want to pay the higher ever-increasing monthly premiums of a Medicare Supplement.

**Medicare Advantage PFFS are not to be confused with Medicare Supplements!**

Here are some Pros and Cons of Medicare Advantage PFFS:

PROS

- A Very large network. As long as the doctor accepts the rate then you’ll be covered.

- Lower monthly premiums than most Medicare Supplements.

- Some plans include Part D prescription drug coverage.

- Maximum out of pocket limit to keep your costs low every year.

- No need for referrals.

- No need to select a Primary Care Physician.

CONS

- Higher premiums, copayments, coinsurance, deductibles than HMO or PPO.

- Can be a hassle to find out if doctor accepts PFFS rate or not.

- Generally fewer and less additional benefits beyond what Original Medicare covers compared HMO, PPO.

As you can see, there are many types of Medicare Advantage plans. Determining which is the right fit for you can be a daunting task on your own.

Let our ‘Even Better’ Medicare plan experts help you figure this out! We’re here to answer any and all questions you have and help guide you on your Medicare journey!

Browse Page