Even Better Insurance

Medicare Part D Donut Hole

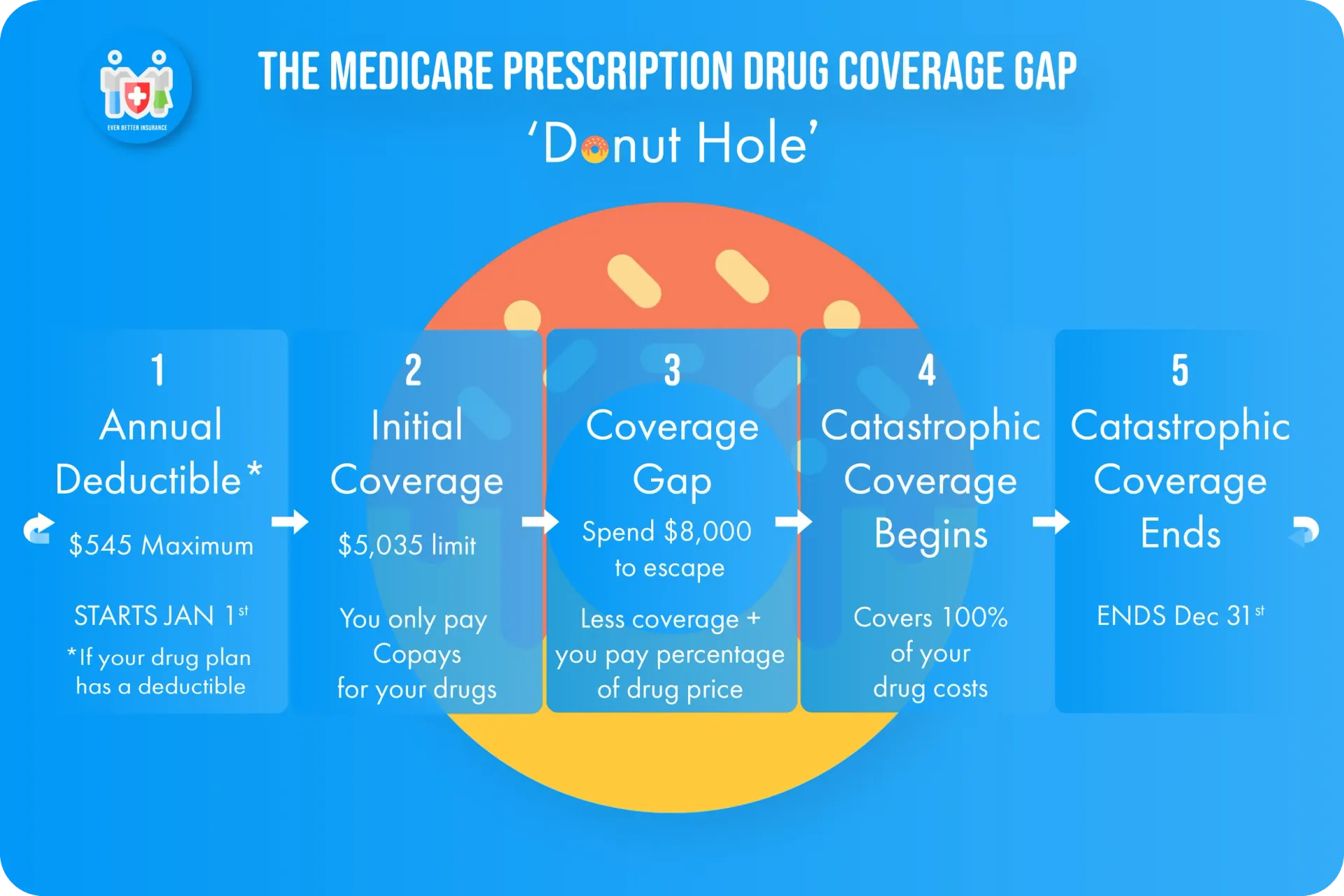

The Prescription Drug Coverage Gap aka “The Donut Hole”

The Medicare prescription drug 'coverage gap’, or ‘donut hole’, is a confusing and often misunderstood topic among those new to Medicare and existing beneficiaries alike. To fully understand the coverage gap, you must first understand all of the stages of Part D coverage. By the end of this article you’ll be able to understand what the gap is, why it exists, how it is set up and when/if it will affect you. We’ve also included some frequently asked questions that our clients have found useful.

The coverage gap is one of the four stages of coverage. Read on for a detailed explanation of each stage:

Quick Links

Prescription Drug Coverage Stages

1. Annual Deductible

Every year, Medicare updates the standard Part D deductible. In 2024 it is $545, meaning that no Part D drug plan can charge you a deductible higher than $545 this year. In many cases, both stand alone drug plans and drug plans included with Medicare Advantage plans will actually have lower deductibles than the maximum (or no deductible at all) to entice people to join their plan.

If your plan has a deductible, you will begin your coverage in the Annual Deductible stage. During this stage you will be responsible for paying 100% of the retail cost of your drugs until the deductible has been reached. Once you've met your plan’s deductible, you will move to the Initial Coverage stage.

If your plan has a $0 deductible (no deducible) then you will automatically skip the Annual Deductible stage and start in the Initial Coverage stage…

Browse Page

2. Initial Coverage

This is the stage where the plan’s advertised copayments and coinsurance amounts kick in. This stage is the most familiar coverage stage because it acts similar to all other insurance coverages. You have set copayment and coinsurance amounts laid out by the plan that you will pay. In the case of prescription drug coverage, the amounts you’ll pay depend on the drug’s tier rating set forth by the plan. The lower the tier, the cheaper the drug’s copayments are while higher tiers tend to carry higher copayment and coinsurance amounts.

During this Initial Coverage stage, Medicare adds the amounts that both you AND your Part D plan have paid. This essentially means it is easier to spend your way into the Coverage Gap than it is to spend your way out once you’ve entered.

Browse Page

3. The Coverage Gap or 'Donut Hole'

After you reach your Initial Coverage limit, you will enter the Coverage Gap stage or ‘Donut hole’ - a period of time in which you pay higher cost sharing for prescription drugs until you spend enough to qualify for Catastrophic Coverage. In 2024, you need to be credited $8,000 in True out of pocket costs (Troop) to escape the Coverage Gap and reach Catastrophic Coverage. Let’s dive in and take an in-depth look at what this stage is and how you can get through it as fast as possible.

As of 2024, while you are in the Coverage Gap stage, you are responsible for paying 25% of brand name drug cost and 25% of the generic drug cost. Again, to escape the Coverage Gap this year, you need to spend $8,000 (in 2024) in out-of-pocket costs. How these out-of-pocket costs are counted vary depending on if the drug is a brand-name drug or if it is a generic drug:

Brand-name drugs in the Coverage Gap

In the coverage gap you’ll pay no more than 25% of the cost of your plan’s covered brand name drugs. Some plans may even lower the amount you’ll pay to less than 25%.

Even though you’ll pay no more than 25%, nearly the full retail price of that drug will count as a qualifying out-of-pocket cost to help you get out of the Coverage Gap. What you pay and what the manufacturer pays (95% of the cost of the drug) will count toward your out-out-pocket spending. Here's a breakdown:

- Out of the retail cost of the drug, the manufacturer pays 70% of the cost in order to discount the price for you further. Then your Part D plan pays 5% of the cost, which equals 75% of the cost for that drug. You are responsible for paying the remaining 25%.

- On top of that 100% cost of the drug, the pharmacy also charges a dispensing fee. Your plan pays 75% of that fee, and you pay 25% of it.

- **The drug plan’s 5% share of cost and its 75% share of the dispensing fee DO NOT count towards your out-of-pocket limit.**

Example: Mr. Smith has just entered the Coverage Gap this year. He goes to his pharmacy to fill a prescription for a covered brand name drug he’s taking. The price of the drug is $80 and there’s a $2 dispensing fee that gets added to the costs, making the total price $82. Mr. Smith pays 25% of that total cost ($82 x .25 = $20.50).

The amount Mr. Smith pays, $20.50, and the amount the manufacturer paid to discount this drug ($80 x .70 = $56) both count towards Mr. Smith’s out-of-pocket expenses so he will be credited ($20.50 + $56 = $76.50) $76.50 towards the 2024 Coverage Gap limit of $8,000.

The 5% of the cost your plan pays for the drug (in this case 5% of $80 = $4), and the 75% dispensing fee your plan pays (let’s say it was $3.50) DO NOT count towards your out-of-pocket expenses.

**If you have a Medicare drug plan that already includes coverage in the gap, you may get a discount after your plan's coverage has been applied to the drug's price. The discount for brand-name drugs will apply to the remaining amount that you owe.**

Generic drugs in the Coverage Gap

Medicare will pay 75% of the price for generic drugs during the coverage gap. You'll pay the remaining 25% of the price. The coverage for generic drugs works differently from the discount for brand-name drugs. For generic drugs, only the amount you pay will count toward getting you out of the coverage gap.

Example: Mrs. Robinson has just entered the Coverage Gap. She goes to the pharmacy to fill a prescription for her covered generic drug. The price of this drug is $15, and there is a $1 dispensing fee for a total of $16. Mrs. Robinson will pay 25% of the plan’s cost for the drug as well as the dispensing fee ($16 x .25 = $4). The $4 she paid will be counted towards her out-of-pocket expenses and get her closer to escaping the Coverage Gap.

**If your drug plan already includes coverage in the gap, you may get a further discount after your plan's coverage has been applied to the drug's price.**

We hope these examples of how those out-of-pocket expenses are counted will help you plan for the period leading up to the Coverage Gap, the Coverage Gap, and for when you escape the Coverage Gap and enter the much more financially friendly Catastrophic Coverage stage.

Browse Page

4. Catastrophic Coverage

Once you escape the Coverage Gap, you’ll immediately enter the Catastrophic Coverage stage. Despite the name, the Catastrophic Coverage stage is often a period of welcome respite for those taking expensive medications. That is because once you reach Catastrophic Coverage, your Part D plan increases its own cost-sharing percentage which dramatically decreases the amount you must pay for your covered drugs for the remainder of the year. In 2024, you will pay no cost in the catastrophic coverage stage for a covered drug for the rest of the year.

Browse Page

Common Coverage Gap Questions

Will I enter the Part D coverage gap?

You will likely enter the coverage gap if your drugs have a combined retail cost over $335 per month. Remember, you’ll enter the coverage gap once your drug costs exceed the standard Initial Coverage limit set by Medicare ($5,035 in 2024).

I’m in the Coverage Gap, what costs count towards getting me out of it?

This is the second most asked question we get asked about Part D plan coverage stages. This subject is confusing because the costs that are used to determine your Initial Coverage limit are different from the ones used to determine when you’ll spend your way out of the Coverage Gap. As noted above, it also depends on whether you are taking brand name drugs or generic drugs.

Here is a short list of what does and does not count towards escaping the Coverage Gap:

What DOES count:

- Your yearly drug deductible, coinsurance, and copayments.

- The discount you receive on brand-name drugs while you’re in the gap. This is the amount the manufacturer pays on your behalf to reduce the retail cost of the drug (70%).

- What you pay for covered drugs while in the gap.

What DOES NOT count:

- Your Part D plan’s monthly premium.

- Pharmacy dispensing fee

- What you pay for drugs that are not covered by your drug plan.

If you need to dispute a discount you may be owed according to your drug plan, you can learn about how to file an appeal via Medicare.gov.

How can I lower my drug costs while in the Coverage Gap or ‘Donut Hole’?

Being the in coverage cap can be a financially difficult and stressful time. Here are a few ways you may be able to lower your costs even further:

- Opt-in for your plan’s 90-day mail order delivery when possible. Drug plans often give you discounts when you get your drugs through the mail and in large quantities because it ensures less missed doses and less chances you’ll run out of necessary medications.

- Ask your doctor about generic alternatives to your brand name drugs.

- Use Medicare.gov’s pharmaceutical assistance program finder tool: https://www.medicare.gov/pharmaceutical-assistance-program/

- Use Medicare.gov’s pharmaceutical state-based assistance program finder tool: https://www.medicare.gov/pharmaceutical-assistance-program/#state-programs

- Retail discount programs. These are discount programs offered by retail pharmacies in the form of coupons etc that may help you save even more on drug prices during the coverage gap. Keep in mind however, that many times these discount programs have ‘fine print’ that state they cannot be used in tandem with your Part D plan. Make sure you understand any restrictions.

How do my drug costs determine when I will hit my Initial Coverage stage limit?

Determining which costs are factored in to the various Part D coverage stages can be confusing. This is the most common question that beneficiaries ask.

The retail price your Prescription drug plan negotiates with manufacturers is the ‘retail price’ that counts towards your Initial Coverage limit. This price can be found in the monthly document your drug plan sends you called an ‘explanation of benefits’.

What if my pharmacy’s retail price for a drug is cheaper than my Part D plan’s copayment or coinsurance price?

Simple. You’ll pay the cost of your pharmacy’s lower retail price instead of your Part D plan’s copay. For example: If your local network pharmacy charges $15 for a drug that your Part D plan charges a $30 copayment for, then you will want to purchase that drug paying your pharmacy’s retail price instead.

Will I have to restart any/all of the coverage stages if I switch Part D Plans during the year?

No. Even though you have benefits through one insurance plan or another, your record of costs is tracked by Medicare itself. So, that means if you switch prescription drug plans, you will not be subject to more than one Part D deductible, or have several instances of the Initial Coverage stage, Coverage Gap or Catastrophic Coverage.

Need help understanding the Coverage Gap or how to avoid it? Curious about what your drugs will cost you this year? For personalized answers to that and every other Part D question, contact our friendly and knowledgable ‘Even Better’ Medicare plan experts today!

Browse Page